Define your settlement requirements

Before writing a single line of smart contract code, determine exactly how your stablecoin will be used. The architecture of your private infrastructure depends entirely on the specific business use case. Are you building a system for internal treasury management, cross-border vendor payments, or payroll distribution? Each scenario demands a different balance of privacy, speed, and regulatory compliance.

For internal treasury operations, the primary goal is often efficiency and auditability rather than public anonymity. You need to reconcile on-chain balances with your internal accounting records, ensuring that anti-money laundering (AML) and sanctions workflows are embedded directly into the transaction flow. In this context, "privacy" means restricting data access to authorized internal parties, not hiding transactions from regulators.

If your use case involves cross-border payments or institutional counterparties, the requirements shift. You may need "need-to-know" privacy, where specific details like pricing, counterparty identities, or trading strategies are visible only to the relevant parties involved in a transaction. This approach allows stablecoins to move freely on public or permissioned blockchains without exposing sensitive commercial information to the broader network. As noted by Canton Network, this programmable privacy enables settlement at institutional scale while maintaining composability.

Map out your transaction volume and counterparty types early. High-volume, low-value payments (like payroll) require different optimization than low-volume, high-value settlements (like M&A financing). This initial definition stage prevents costly architectural changes later when you realize your chosen ledger or oracle system cannot handle your specific compliance or throughput needs.

Select the underlying blockchain network

Choosing the right ledger is the first structural decision in building private stablecoin infrastructure. You are essentially deciding who gets to see the transaction data and how quickly it settles. Public blockchains like Ethereum or Solana offer transparency, while permissioned ledgers like Hyperledger Fabric or R3 Corda restrict access to authorized participants. For private assets, this distinction determines whether your counterparty data remains confidential or becomes public record.

The choice often comes down to a trade-off between composability and privacy. Public chains allow your stablecoin to interact with decentralized finance (DeFi) protocols, but every transaction is visible to anyone running a node. Permissioned networks keep data within a closed consortium, offering "need-to-know" privacy for institutional payments, but they sacrifice the open programmability of the public internet. If you need to settle vendor payments or payroll without exposing strategies, a permissioned ledger may be the safer bet.

Use the comparison below to weigh the operational realities of each option. This isn't just about technology; it's about regulatory alignment and data visibility.

| Feature | Public Blockchain | Permissioned Ledger |

|---|---|---|

| Data Visibility | Transparent to all nodes | |

| Data Visibility | Restricted to authorized parties | |

| Transaction Finality | Seconds to minutes | |

| Transaction Finality | Seconds to hours | |

| Regulatory Alignment | Evolving, mixed | |

| Regulatory Alignment | High, enterprise-ready | |

| Composability | High (DeFi integrations) | |

| Composability | Low (closed ecosystem) |

For many finance professionals, the decision hinges on whether the stablecoin needs to interact with the broader crypto economy or stay within a corporate silo. If you are building for internal treasury management, a permissioned ledger reduces regulatory friction. If you are building for public issuance with privacy features, you might look at hybrid approaches that layer privacy protocols on top of public chains.

As an Amazon Associate, we may earn from qualifying purchases.

Embed compliance and monitoring into the settlement flow

You cannot treat compliance as an afterthought. When you build private stablecoin infrastructure, AML, Know Your Customer (KYC), and sanctions screening must happen inside the settlement flow. If these checks happen after the transaction settles, you are already moving illicit funds. Stripe notes that stablecoin infrastructure includes the systems that handle identity checks and onchain transaction analysis to reconcile balances with internal records.

The goal is to verify the actor and the asset before the transfer executes. This requires integrating offchain compliance data with onchain settlement logic. You need to screen wallet addresses against sanctions lists and verify identity tokens before minting or transferring stablecoins.

Require KYC data before a user can mint stablecoins. Use an identity provider to verify the user’s legal identity. Store the verification result as a signed attestation. Your smart contract should only allow minting if this attestation is valid. This ensures every token has a known, verified owner from the start.

Connect your settlement API to a sanctions screening provider. Before any transaction is signed, screen both the sender and receiver wallet addresses. Block the transaction if either address appears on a sanctions list like OFAC. This prevents your platform from processing payments for prohibited entities. Do this synchronously to avoid delays.

Not all transactions are equal. Implement a risk scoring engine that analyzes transaction patterns. Flag high-risk behaviors, such as rapid transfers between unverified wallets or interactions with known mixers. Use this data to trigger enhanced due diligence. This monitoring should run in parallel with settlement, not as a bottleneck.

Embed the compliance logic directly into your smart contract. Use access control lists to restrict minting and burning to verified addresses. Implement pause functions that can freeze assets if suspicious activity is detected. This ensures that even if your API fails, the onchain rules still protect your infrastructure.

Maintain a private ledger that mirrors onchain activity. Reconcile this ledger with your internal KYC/AML records daily. This ensures you have a complete audit trail for regulators. It also helps you identify discrepancies between onchain activity and your internal risk models.

By embedding these checks, you build a system that is both compliant and private. You protect your platform from regulatory risk while maintaining the speed and efficiency of stablecoin settlements.

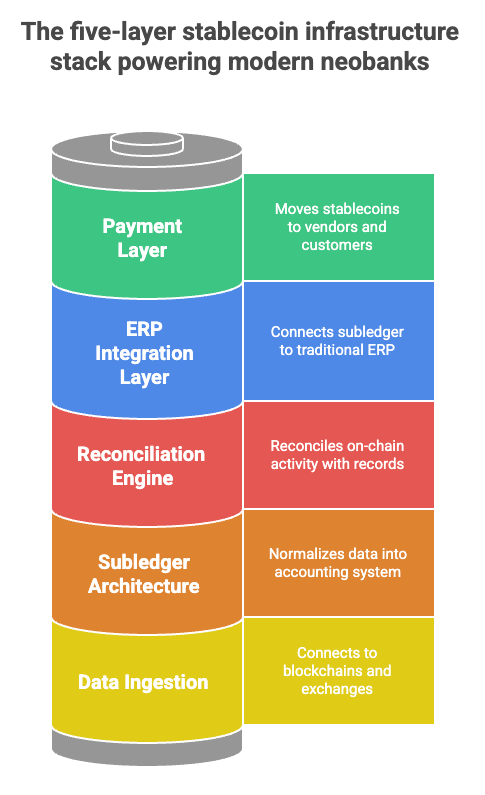

Connect to existing financial systems

Linking your stablecoin rails to legacy banking and ERP software requires more than just a blockchain bridge. You need middleware that translates on-chain events into the structured data formats banks and accounting systems expect. This integration ensures that when a stablecoin transaction settles, your internal ledgers and traditional banking records update in real time.

The first step is establishing a reliable API layer. Platforms like Bridge provide end-to-end stablecoin infrastructure, offering APIs that handle receiving, storing, and converting assets while managing the underlying compliance workflows. These APIs act as the translator between your private blockchain and the outside world, ensuring that transaction data is formatted correctly for external systems. You should prioritize middleware that supports standard financial messaging protocols, allowing your stablecoin operations to talk directly to SWIFT or ACH networks without custom code for every bank.

Reconciliation is where most integrations fail. Stablecoin infrastructure must include tools that reconcile on-chain balances with internal records and traditional bank statements. Since stablecoins touch regulated financial systems, your middleware must handle identity checks, fraud screening, and AML workflows automatically. If your system cannot prove that a digital token matches a fiat deposit in a bank account, auditors will flag it immediately. Build error-handling protocols that pause transactions when discrepancies arise, rather than letting them drift into your general ledger.

-

Verify API endpoints for SWIFT/ACH translation

-

Test reconciliation logic with testnet transactions

-

Configure error handling for failed bank withdrawals

-

Audit AML and sanctions screening workflows

Test settlement flows before launch

Testing settlement flows requires moving beyond theoretical comparisons to validate day-to-day operational constraints. A choice can look strong on paper and still fail because it is too hard to maintain, too expensive to repeat, or awkward in the actual setting.

Use a consistent checklist for every option: fit, cost, durability, timing, upkeep, and fallback plan. That keeps the comparison practical instead of drifting into preference alone. The simplest way to use this section is to write down the real constraint first, compare each option against it, and choose the path that still works outside ideal conditions.

No comments yet. Be the first to share your thoughts!