Map your settlement requirements

Before selecting a technology stack, you must define the specific B2B use case driving your private stablecoin implementation. Whether you are building cross-border payment rails or supply chain finance solutions, the operational requirements for privacy and speed will differ significantly. This initial mapping determines whether your infrastructure needs to prioritize low-latency finality or strict counterparty confidentiality.

Private stablecoins hide counterparty data on public ledgers, essential for protecting trade secrets in B2B deals.

For cross-border payments, the primary constraint is often speed and cost reduction compared to traditional correspondent banking. Stablecoins can be sent between two blockchain-based wallet addresses without their owners opening an account at a financial institution, bypassing the delays inherent in legacy banking networks McKinsey. In this scenario, your requirement map should focus on transaction throughput and liquidity management across jurisdictions.

Conversely, supply chain finance often demands higher levels of privacy. Companies may need to issue and access stablecoins that move freely without exposing pricing, counterparties, or commercial strategies Canton Network. Here, the tech stack must support programmable privacy features that keep sensitive trade data off the public record while maintaining composability with other financial services.

Clarifying these distinctions early prevents over-engineering. A system built for high-frequency cross-border settlements may lack the granular access controls needed for confidential supply chain contracts, and vice versa. By anchoring your design to these specific operational goals, you ensure the resulting infrastructure is both compliant and efficient.

Select a compliant issuance model

Choosing between a private stablecoin issuance model and a third-party provider is a structural decision that defines your regulatory exposure. The choice hinges on your organization's capacity to manage legal compliance versus the desire for immediate operational simplicity.

Build your own ledger

Issuing your own token on a permissioned ledger places you in the role of a regulated financial institution. This path offers complete control over the reserve assets and the ability to design custom compliance rails tailored to specific B2B workflows. However, it requires significant upfront investment in legal counsel, licensing, and ongoing audit infrastructure. You become directly responsible for Anti-Money Laundering (AML) checks, sanctions screening, and reserve attestations.

This approach is viable if you have the capital to absorb regulatory risk and the technical expertise to maintain a compliant blockchain node. You are building a long-term asset, but the time-to-market is measured in quarters or years, not weeks.

Use a third-party provider

Alternatively, you can integrate with established stablecoin infrastructure providers like Fireblocks or Stripe. These platforms handle the complex backend requirements, including custody, compliance monitoring, and on-chain reconciliation. You gain access to stablecoin settlement rails without becoming a regulated issuer yourself. This model shifts the compliance burden to the provider, allowing your team to focus on the application layer and customer experience.

While this option reduces initial legal overhead, it introduces vendor dependency and potential integration constraints. You must ensure the provider's risk controls align with your B2B partners' requirements.

| Feature | Self-Hosted / Issuer | Third-Party Provider |

|---|---|---|

| Regulatory Burden | High (Direct licensing & audit) | Low (Provider handles compliance) |

| Control over Reserves | Full control | Dependent on provider terms |

| Time to Market | Months to years | Weeks |

| Development Cost | High (Infrastructure & legal) | Moderate (Integration fees) |

| Customization | Unlimited | Limited to API capabilities |

Decision checklist

Before committing to a model, verify your regulatory footprint. If you plan to hold customer funds or issue tokens directly, you likely need a money transmitter license or equivalent. If you only need to accept or send stablecoins for internal settlements, a provider-led model is often sufficient. Evaluate your internal engineering team's capacity to maintain blockchain nodes and their ability to respond to rapid regulatory changes in your target jurisdictions.

Integrate compliance and risk controls

Embedding AML, KYC, and sanctions screening directly into your private stablecoin settlement rails is not optional for high-stakes finance. Regulators expect these checks to happen before assets move, not after. By weaving compliance into the transaction flow, you prevent frozen funds, regulatory fines, and operational bottlenecks.

Stripe notes that stablecoin infrastructure must include monitoring tools for identity checks, fraud screening, and onchain transaction analysis to reconcile balances with internal records. This means your smart contracts or settlement layer should reject transactions that fail these checks automatically. Here is how to build that sequence.

Capture the sender’s verified identity (KYC) and transaction details at the point of initiation. Do not allow anonymous transfers. Store the hash of the identity verification result on-chain or in a secure off-chain ledger linked to the transaction ID. This creates an immutable audit trail from the start.

Before the transaction is signed, route the counterparty addresses and amounts through an automated screening engine. Check against OFAC lists, EU sanctions, and internal blacklists. If a match is found, the system should halt the transaction and flag it for manual review. This step ensures you are not moving funds for sanctioned entities.

Assign a risk score to the transaction based on screening results, transaction size, and counterparty history. Set clear thresholds: low-risk transactions auto-approve, while medium-risk ones require secondary approval from a compliance officer. High-risk transactions are automatically rejected. This balances speed with security, ensuring legitimate payments move quickly while suspicious ones are caught.

Once approved, execute the stablecoin transfer on the blockchain. Immediately log the transaction hash, compliance status, and timestamp in your internal reconciliation system. This allows your finance team to match on-chain activity with off-chain books. Regular audits of these logs ensure you remain compliant with evolving regulatory standards.

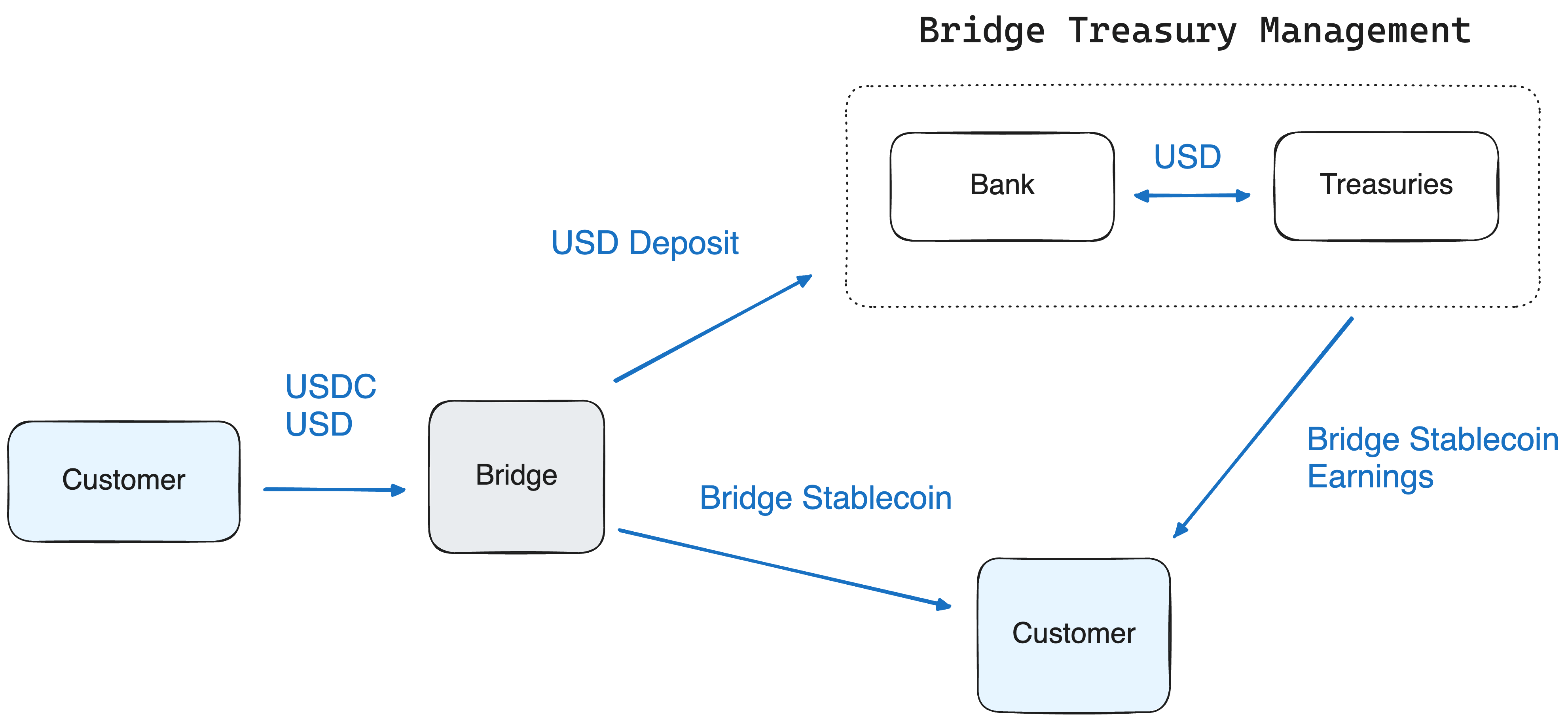

Connect liquidity and settlement rails

To settle transactions in fiat or stablecoins with minimal slippage, you must bridge the onchain ledger with offchain banking rails. This connection relies on direct bank APIs or decentralized oracles that provide real-time price feeds, ensuring that the value transferred matches the value settled.

Establish direct connections to custodial banks or payment processors. This allows your infrastructure to move fiat currency in and out of stablecoin reserves without relying on third-party exchanges, reducing counterparty risk and settlement latency.

Use decentralized oracle networks to monitor stablecoin pegs against the US dollar. These feeds provide the necessary data to adjust liquidity positions dynamically, preventing slippage during periods of market volatility or depegging events.

Build systems that reconcile onchain balances with internal bank records. This ensures that every stablecoin minted or burned corresponds to an actual fiat deposit or withdrawal, maintaining transparency and regulatory compliance.

The scale of this infrastructure is evident in the rapid growth of the market. The global fiat-backed stablecoin supply exceeded $273 billion in March 2026, growing 40x from $6.8 billion in March 2020 according to Allium and Visa data. This expansion underscores the need for robust, low-latency settlement rails that can handle high volumes without compromising accuracy.

Morgan Stanley notes that by being pegged to the dollar and integrated into programmable infrastructures, stablecoins offer real-time settlement and low transaction costs. To achieve this, your system must treat liquidity not as a static pool, but as a dynamic flow that responds to market conditions through automated, API-driven mechanisms.

Audit and monitor transaction flows

Continuous monitoring is the difference between a functional stablecoin rail and a compliance liability. You cannot rely on end-of-day batch reports to catch fraud or sanction violations. Instead, you need real-time visibility into every transaction from minting to redemption.

Start by integrating onchain analysis tools that flag high-risk addresses immediately. These systems should screen against global sanctions lists and known illicit entities before a transaction settles. This layer of defense protects your infrastructure from being exploited for money laundering or terrorist financing.

Next, establish an immutable audit trail that reconciles onchain balances with your internal records. Discrepancies between your ledger and the blockchain are the first sign of a system error or security breach. Automated reconciliation ensures that your reserves are always fully backed and verifiable.

Finally, configure alerts for anomalous patterns. Sudden spikes in volume, transfers to new high-risk jurisdictions, or unusual token movements should trigger immediate review. This proactive approach allows you to pause suspicious activity before it impacts your partners or regulators.

-

KYC integration with real-time screening

-

Wallet security with multi-signature controls

-

Oracle reliability for price feeds

-

Exit liquidity buffers for redemption

Frequently asked questions about private stablecoin infrastructure

What is stablecoin infrastructure?

Stablecoin infrastructure is the underlying technology stack that keeps digital tokens pegged to a real-world asset, typically the US dollar. It combines smart contracts, oracle networks for price feeds, and off-chain systems to ensure reliable transfers. Because these tokens interact with regulated banking systems, the infrastructure also includes compliance layers for identity checks, fraud screening, and Anti-Money Laundering (AML) workflows Stripe.

What is a private stablecoin?

A private stablecoin is a cryptocurrency issued by a non-governmental entity, such as a corporation or consortium, rather than a central bank. These tokens are designed to maintain a fixed value against a fiat currency, effectively acting as a digital dollar. While they offer speed and programmability, they carry inherent risks because their value relies on the issuer's reserves and regulatory standing WSJ.

How do private stablecoins differ from public ones?

Private stablecoins are issued by specific entities and often operate within permissioned networks or closed ecosystems, whereas public stablecoins like USDC or USDT are available on open blockchains to anyone. Private rails allow for greater control over transaction limits, user verification, and integration with existing enterprise software. This makes them better suited for B2B settlement where counterparty risk must be managed through known identities rather than anonymous on-chain analysis.

What are the main risks of using private stablecoin rails?

The primary risks involve counterparty trust and regulatory uncertainty. Since the issuer controls the underlying reserves, there is a risk that the peg could break if the issuer fails to maintain adequate liquidity. Additionally, regulatory frameworks for private money are still evolving, which could impact the token's legality or interoperability with traditional banking systems. Businesses must perform rigorous due diligence on the issuer's audit practices and legal structure.

Why do enterprises prefer private stablecoin infrastructure?

Enterprises often choose private rails because they offer predictable transaction costs and faster settlement times compared to traditional cross-border wire transfers. Private infrastructure allows for direct integration with existing ERP and treasury management systems, enabling automated reconciliation. This reduces the operational friction of manual accounting while providing the transparency of blockchain technology within a controlled, compliant environment.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

- Good starting point

- Matches the article topic

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!