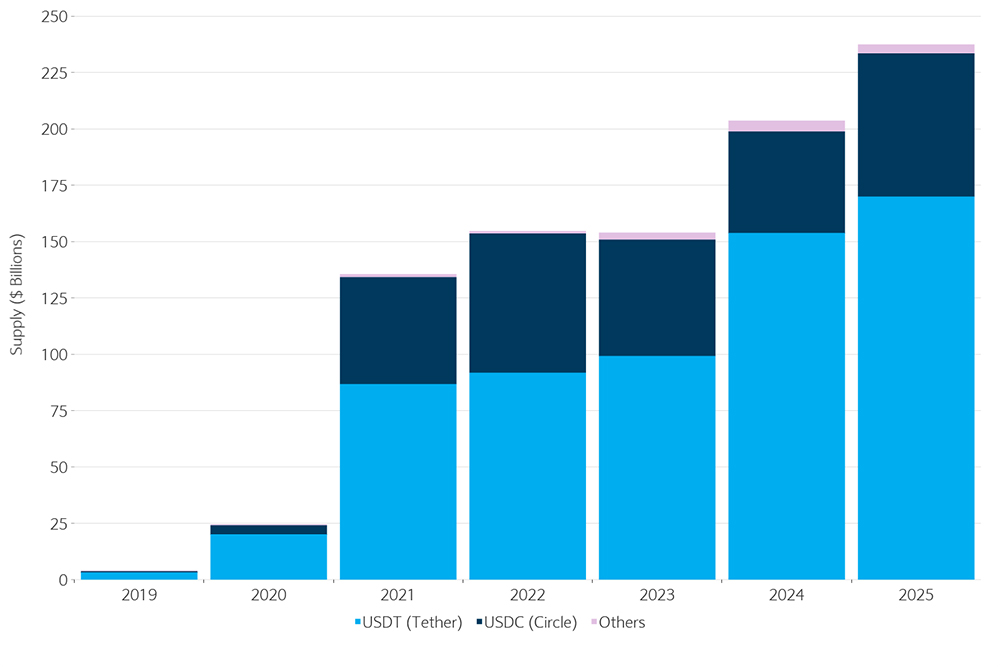

The private stablecoin strategy limits to account for

A private stablecoin strategy is not about launching a new currency; it is about solving the tension between regulatory compliance and operational efficiency. Public stablecoins offer liquidity and transparency but expose institutional balance sheets to public ledger visibility and smart contract risk. Private stablecoins reverse this equation: they allow institutions to tokenize deposits or reserves on public infrastructure while keeping ownership data and transaction details off-chain or permissioned.

This constraint defines the entire architecture. You are not choosing between public and private rails; you are choosing which data stays private and which settlement layer remains public. The strategy hinges on three practical tradeoffs that determine whether the infrastructure holds up under audit.

Permissioned issuance on public rails

The most common private stablecoin model issues tokens on public blockchains like Ethereum or Solana but restricts minting and redemption to authorized entities. This allows the token to be used in DeFi or cross-border payments while ensuring only vetted participants can create or destroy supply. The constraint here is that the public blockchain still records the token address and balance, even if the underlying identity is hidden behind a zero-knowledge proof or a private layer. This approach works best for treasury management where liquidity is paramount but counterparty risk must be strictly controlled.

Off-chain data, on-chain settlement

Institutional stablecoins often keep the "who" and "why" of transactions off-chain while using public chains for final settlement. This means the blockchain acts as a neutral clearinghouse rather than a public ledger of record. The constraint is that you need a robust oracle or bridge system to verify that off-chain balances match on-chain token movements. Without this, you reintroduce the very counterparty risk private stablecoins aim to eliminate. Canton Network and similar platforms enable this by allowing participants to share only the data necessary for settlement, keeping commercial secrets intact.

Regulatory alignment as a feature, not a bug

Private stablecoins must be designed to satisfy local financial regulations from day one. This means embedding KYC/AML checks into the token standard itself, often through non-transferable identifiers or compliant transfer functions. The constraint is that this reduces the token’s utility in open DeFi protocols that require permissionless transfers. The strategy succeeds only if the target use case—such as B2B payments, real-time gross settlement, or internal treasury transfers—does not require open-market liquidity. If the goal is broad consumer adoption, a private stablecoin is the wrong tool; if the goal is institutional efficiency, it is the only viable path.

Private stablecoin strategy choices that change the plan

Choosing a private stablecoin approach requires balancing regulatory compliance, liquidity, and operational control. Public stablecoins offer immediate accessibility but expose institutions to counterparty and smart contract risks. Private stablecoins, often issued as deposit tokens or restricted digital assets, provide tighter governance and privacy but introduce complexity in interoperability and settlement speed.

The decision hinges on your institution’s risk appetite and regulatory jurisdiction. A strategy that works for a global treasury team may fail for a regional payments provider. Below, we compare the core tradeoffs across four critical dimensions to help you evaluate which model aligns with your infrastructure and settlement goals.

| Factor | Public Stablecoins | Private Stablecoins | Hybrid/Tokenized Deposits |

|---|---|---|---|

| Regulatory Clarity | High for major issuers (USDC, USDT); ambiguous for smaller projects | Defined within banking frameworks; depends on local central bank rules | Evolving; often treated as traditional liabilities with blockchain settlement |

| Privacy & Data Control | Transparent ledger; all transactions visible on-chain | Permissioned access; transaction data hidden from public view | Selective disclosure; visible to authorized participants only |

| Liquidity & Settlement | Instant, 24/7 global settlement; deep liquidity pools | Slower; limited to closed networks or specific partners | Near-instant within consortium; slower for external transfers |

| Counterparty Risk | Exposure to issuer solvency and reserve quality | Exposure to issuing bank’s balance sheet and regulatory status | Shared risk; depends on both issuer and network governance |

| Interoperability | High; widely supported by exchanges and DeFi protocols | Low; requires bridges or specific gateway solutions | Moderate; improving with CBDC and tokenized deposit standards |

When evaluating these options, consider the cost of integration. Public stablecoins require minimal setup but carry reputational risk if the issuer faces scrutiny. Private stablecoins demand significant infrastructure investment but offer greater control over compliance and data sovereignty. Hybrid models, such as tokenized deposits on permissioned ledgers, sit in the middle, offering a path to modernization without abandoning traditional banking safeguards.

Your strategy should also account for network effects. If your partners and customers are already using public stablecoins for cross-border payments, a private alternative may create friction. However, if privacy and regulatory certainty are paramount, a private or hybrid approach may justify the added complexity. The goal is not to pick the "best" technology, but the one that best fits your institution’s specific risk and operational profile.

Build a Private Stablecoin Strategy

Choosing how to deploy private stablecoins requires matching the asset’s structure to your specific operational needs. There is no single best approach; the right choice depends on whether you prioritize settlement speed, regulatory compliance, or counterparty privacy.

Use this decision framework to evaluate your options. Each step addresses a core component of the infrastructure, from tokenization to final settlement.

Determine where the final settlement occurs. Public blockchains offer transparency and liquidity but expose transaction data. Private ledgers or permissioned channels (like Canton Network) provide confidentiality for institutional participants. Choose public chains for broad market access and private channels for sensitive treasury operations.

Decide between algorithmic, fiat-collateralized, or hybrid models. Fiat-collateralized tokens backed by commercial paper or cash are the standard for private use cases due to their stability. Ensure the reserve assets are auditable and that the custodian is regulated. Avoid algorithmic models for core treasury holdings due to volatility risks.

Implement identity verification and access controls. Private stablecoins often use whitelisted addresses to ensure only verified entities can hold or transfer the asset. This reduces regulatory risk and prevents illicit flows. Integrate KYC/AML checks directly into the smart contract or the issuing platform’s API.

Connect your stablecoin holdings to your traditional finance (TradFi) infrastructure. Use APIs to reconcile on-chain balances with off-chain general ledgers. This ensures that your internal reporting remains accurate and that you can easily convert stablecoin reserves back to fiat for payroll or vendor payments.

Stay updated on evolving regulations in your jurisdiction. The EU’s MiCA and the US’s stablecoin legislation proposals will impact reserve requirements and issuance rules. Build flexibility into your strategy so you can adjust your token provider or settlement layer if compliance standards shift.

As an Amazon Associate, we may earn from qualifying purchases.

Avoid Weak Stablecoin Options

Many teams chase stablecoin utility without auditing the underlying settlement layer. This section flags the most common structural failures in private stablecoin strategies, from opaque reserve audits to fragile peg mechanisms.

Opaque Reserve Audits

Public blockchains require public transparency. If a stablecoin issuer relies on quarterly PDF reports instead of real-time on-chain proofs, you cannot verify liquidity during a stress event. Treat any asset without daily, verifiable reserve attestations as high-risk counterparty exposure.

Fragile Peg Mechanisms

Algorithmic or hybrid pegs often fail under low-volume conditions. Look for stablecoins that use direct arbitrage incentives or over-collateralized debt positions rather than complex seigniorage shares. If the peg requires constant market intervention, it is not a stable base asset.

Regulatory Arbitrage Traps

Issuers based in jurisdictions with no clear stablecoin framework expose users to sudden freezing or seizure risks. Prioritize issuers subject to recognized banking or payment regulations. The lack of legal clarity is a silent killer for institutional adoption.

Poor Interoperability

A stablecoin that only works on one chain limits your strategy. Ensure the asset supports standard bridging protocols and multi-chain settlement. If you cannot move it freely between Ethereum, Solana, or private ledgers, its utility is artificially capped.

Private stablecoin strategy: what to check next

Before committing capital or infrastructure, it helps to separate marketing claims from operational reality. The following answers address the most common objections regarding regulatory alignment, technical flexibility, and market positioning.

No comments yet. Be the first to share your thoughts!