Map your settlement requirements

Before selecting a protocol, define the specific friction points in your current B2B payment flows. Private stablecoin infrastructure is not a general-purpose crypto play; it is a targeted solution for speed, cost, and privacy. Generic public ledgers often fail to meet institutional standards because they expose counterparty identities and trading strategies to the entire network.

Your requirements typically fall into three buckets. First, speed: can your current system settle cross-border vendor payments in seconds rather than days? Second, cost: are you absorbing high FX fees and intermediary bank charges that erode margins? Third, privacy: do you need to keep transaction volumes and counterparties confidential from competitors and the public?

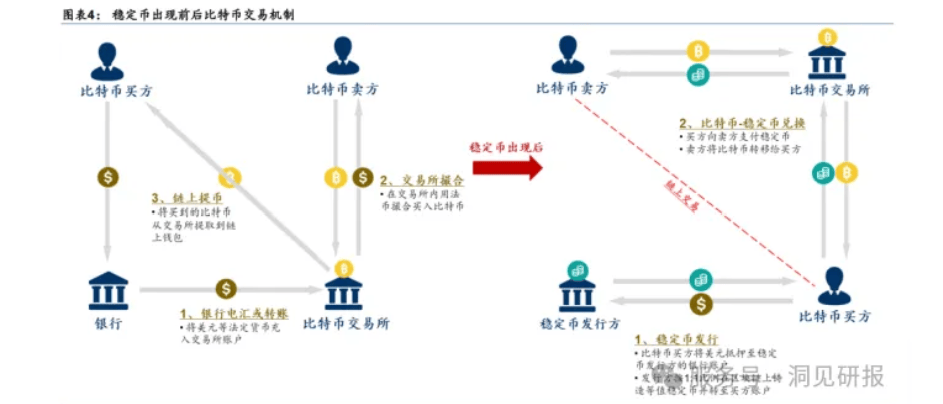

McKinsey notes that stablecoins can be sent between wallet addresses without requiring either party to open a traditional financial institution account, bypassing legacy banking bottlenecks. However, privacy-enabled solutions like those on Canton Network allow you to maintain "need-to-know" visibility. This means you settle payments and streamline payroll without exposing amounts or strategies to the broader market. Define these needs clearly to ensure your infrastructure choice matches your operational reality.

Select the right blockchain layer

Choosing the underlying ledger for your private stablecoin infrastructure is a foundational decision. You are balancing the need for institutional-grade privacy against the liquidity and interoperability of broader networks. The choice generally falls between public chains with privacy layers and permissioned ledgers.

Public blockchains offer deep liquidity and composability, which are essential for cross-border B2B settlements. However, standard public ledgers expose transaction data to everyone. To address this, newer architectures like Canton Network allow stablecoins to move freely without exposing pricing, counterparties, or strategies. This "programmable privacy" enables settlement at institutional scale while maintaining the benefits of a public network Canton Network.

Alternatively, permissioned ledgers (private blockchains) restrict access to known entities. This structure aligns closely with traditional banking compliance frameworks, offering clear regulatory boundaries. While they may lack the open liquidity of public chains, they provide the audit trails and data isolation that many regulated financial institutions require for internal controls.

The table below compares these two approaches across key operational dimensions.

| Layer Type | Privacy Model | Throughput & Cost | Regulatory Alignment |

|---|---|---|---|

| Public (Privacy Layer) | Need-to-know; data hidden from public view | High; low fees; shared network | Evolving; requires careful compliance design |

| Permissioned Ledger | Full access control; known participants only | Variable; often lower than public L1s | High; familiar to traditional auditors |

As an Amazon Associate, we may earn from qualifying purchases.

Your selection should depend on where your counterparties operate and how they view data visibility. If your partners are already on public chains, a privacy layer is the smoother path. If they require strict data silos, a permissioned ledger may be the only viable option.

Integrate compliance and custody tools

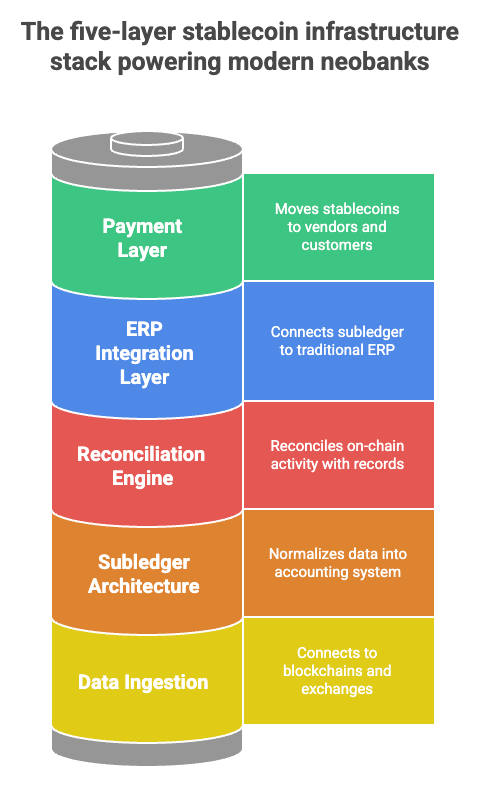

High-stakes B2B settlement requires more than just a token bridge. You need a regulatory backbone that satisfies auditors and protects corporate treasury assets. This section outlines the critical infrastructure components: identity verification, AML screening, and institutional-grade custody.

Before any stablecoin transfer occurs, you must verify the identity of the receiving entity. Standard web2 KYC checks are insufficient for onchain transactions. Integrate a compliance API that validates business registration numbers, beneficial ownership data, and sanctions lists. Stripe notes that stablecoin infrastructure must handle identity checks and fraud screening to maintain steady value and reliable transfers for businesses [[src-serp-4]]. This step ensures your private ledger only interacts with vetted corporate entities.

Anti-Money Laundering (AML) screening is an ongoing process, not a one-time check. Every transfer initiated by your private stablecoin infrastructure must be screened against real-time watchlists. Use automated tools that analyze onchain transaction patterns for suspicious activity, such as rapid movement through mixing services or interactions with sanctioned addresses. This layer protects your organization from regulatory penalties and reputational damage [[src-serp-4]].

For B2B settlements, private keys cannot reside in retail wallets. You need a custody solution that offers multi-signature approval workflows, hardware security modules (HSMs), and clear audit trails. Institutional custodians provide the insurance and compliance reporting required by corporate finance departments. As noted by Bridge, robust infrastructure includes digital wallets and custody layers that are distinct from the payment rails themselves [[src-serp-7]]. This separation ensures that even if the payment interface is compromised, the treasury assets remain secure.

Test the settlement pipeline

Before you route live B2B payments, you must prove that your private stablecoin infrastructure handles finality, reconciliation, and errors without friction. The goal is not just to show that tokens move; it is to demonstrate that the entire ledger remains accurate and compliant under pressure.

Start by simulating high-volume transactions across your network. Verify that on-chain balances reconcile perfectly with your internal accounting records. This step is critical because, as noted by industry experts, stablecoin infrastructure must include robust compliance and monitoring tools that handle identity checks, fraud screening, and AML workflows. If your internal records drift from the blockchain, your settlement pipeline is broken.

Next, stress-test your error handling. Intentionally trigger failed transactions, network timeouts, and partial settlements. Ensure your system automatically rolls back or flags these events without leaving dangling assets or unreconciled entries. You need to confirm that your audit trail captures every state change, providing a clear paper trail for regulators and internal auditors.

Finally, validate the privacy controls. Since your infrastructure is private, ensure that counterparty details, transaction amounts, and strategies remain visible only to authorized parties. Test that your "need-to-know" privacy mechanisms work correctly, preventing data leakage while maintaining the transparency required for settlement finality.

Pre-launch validation checklist

-

Finality Confirmation: Verify that transaction confirmations match your internal ledger within the expected block time.

-

Reconciliation Audit: Run a full audit of on-chain balances against off-chain accounting records to ensure zero drift.

-

Error Rollback: Simulate failed transactions and confirm that assets are returned to the sender or flagged for manual review.

-

Compliance Logging: Ensure all AML, KYC, and sanction screening results are permanently recorded and immutable.

-

Privacy Isolation: Test that unauthorized users cannot view counterparty identities, amounts, or transaction strategies.

-

Network Resilience: Confirm the system handles network latency or node failures without losing transaction data.

-

Audit Trail Integrity: Verify that every state change, including retries and corrections, is logged with a unique timestamp.

Avoiding Common Integration Mistakes

Building private stablecoin infrastructure is less about writing code and more about managing risk. Many B2B teams treat the blockchain as a simple ledger, ignoring the complex regulatory and operational layers that actually keep the system safe. When you ignore these realities, settlement speed becomes irrelevant because compliance failures halt transactions.

Ignoring Reserve Transparency

A stablecoin is only as trustworthy as its backing. If your private token’s reserves are opaque, enterprise clients will not integrate it into their treasury management systems. You need real-time proof that every token is backed by liquid, audited assets. Without this transparency, you are not building a settlement rail; you are building a liability trap. Morgan Stanley notes that modernizing financial infrastructure requires stablecoins to be pegged securely to the dollar while remaining integrated into programmable systems that offer real-time settlement [Morgan Stanley].

Underestimating Compliance Overhead

Stablecoin infrastructure is not just a payment gateway; it is a compliance engine. You must account for identity checks, fraud screening, Anti-Money Laundering (AML) workflows, and sanctions screening. These are not optional add-ons; they are foundational requirements for any system touching regulated financial data. Stripe emphasizes that infrastructure must include these monitoring tools to reconcile onchain balances with internal records effectively [Stripe]. If your team underestimates this overhead, your integration will fail during the first audit.

Failing to Plan for Cross-Chain Interoperability

B2B settlements rarely stay on a single blockchain. Your infrastructure must handle interoperability from day one. If your private stablecoin cannot move seamlessly across chains or interact with existing ERP systems, you create silos that defeat the purpose of instant settlement. Plan for these connections early, or you will face expensive refactoring later.

Frequently asked questions about private stablecoin infrastructure

What is stablecoin infrastructure?

Stablecoin infrastructure is the set of systems that keep stablecoins functioning by maintaining steady value, reliable transfers, and regulatory compliance. This includes interconnected layers like blockchains, reserves, digital wallets, custody solutions, and payments rails. Since stablecoins touch regulated financial systems, the infrastructure also encompasses compliance and monitoring tools for identity checks, fraud screening, Anti-Money Laundering (AML), and sanctions workflows [src-serp-4].

Is there a private stablecoin?

Yes. Private stablecoins allow institutions to issue and access digital assets that move freely without exposing pricing, counterparties, or trading strategies. Platforms like Canton Network enable "need-to-know" privacy, allowing settlement and payments at institutional scale. This privacy streamlines vendor payments, payroll, and cross-border obligations while keeping sensitive data off the public ledger [src-serp-5].

Why would banks use XRP instead of stablecoins?

The primary driver is capital efficiency. XRP represents "free" capital, whereas stablecoins require "locked" capital. To issue $1 billion in stablecoins, a bank must keep $1 billion in cash or low-yield bonds in reserve to back the issuance. XRP, as a bridge currency, does not require this collateral, freeing up balance sheet capacity for other uses [src-serp-7].

No comments yet. Be the first to share your thoughts!