Define the settlement scope

Private stablecoins are issued by fintechs or enterprises, not governments. They rely on 1:1 fiat reserves and private redemption mechanisms.

Before building infrastructure, define the exact settlement scope. This decision dictates the legal structure, reserve custody, and blockchain architecture. The two primary paths are internal treasury management and cross-border B2B payments.

Internal treasury management

This scope involves using stablecoins to move value between subsidiaries or within a single corporate entity. The goal is usually faster reconciliation and reduced banking fees. Since the users are known and regulated entities, the compliance burden is lower. You can use private, permissioned blockchains or standard public chains with strict wallet whitelisting. The infrastructure focuses on internal accounting integration rather than public-facing user experience.

Cross-border B2B payments

This scope involves settling payments between distinct legal entities across different jurisdictions. Here, the stablecoin acts as a neutral settlement layer. You must account for foreign exchange risks, anti-money laundering (AML) checks for each counterparty, and varying regulatory requirements. The infrastructure must support high-volume, low-latency transactions with robust audit trails. Public chains are often preferred for transparency, but the compliance layer becomes significantly more complex. As noted by a16z crypto, stablecoins enable "new kinds of software" by removing traditional banking friction, but this requires careful legal scoping a16z crypto.

Consumer-facing transactions

If the stablecoin is intended for retail users, the scope expands to include consumer protection laws, chargeback mechanisms, and broader KYC/AML requirements. This path is the most regulated and infrastructure-heavy. Most private stablecoins currently focus on B2B or institutional use to avoid the direct regulatory scrutiny associated with consumer deposits Stripe.

Compare public ledgers against permissioned networks

Choosing the right blockchain is the first structural decision in building a private stablecoin. You are balancing three competing forces: regulatory visibility, transaction cost, and user privacy. Public Layer 1s like Ethereum offer deep liquidity and established compliance tooling but come with high gas fees and transparent on-chain data. Permissioned ledgers, such as Hyperledger Fabric or Quorum, provide privacy and lower costs but require you to build and maintain your own validator infrastructure.

Stripe notes that the choice of infrastructure dictates your compliance burden. Public chains are "permissionless," meaning anyone can interact with them, which requires robust transaction monitoring to prevent illicit activity. Permissioned networks are "closed systems," where only approved entities can participate, simplifying KYC/AML integration but limiting interoperability with the broader crypto economy.

The table below breaks down the core differences. Use this to align your technical choice with your regulatory reporting requirements.

| Feature | Public Layer 1 (e.g., Ethereum) | Permissioned Ledger (e.g., Hyperledger) |

|---|---|---|

| Regulatory Visibility | High (public ledger) | Low (private ledger) |

| Transaction Cost | Variable (gas fees) | Fixed (low) |

| Privacy | Low (transparent) | High (restricted access) |

| Infrastructure | Public nodes | Self-hosted validators |

| Compliance Integration | Requires external monitoring | Built-in access control |

For most high-stakes financial applications, permissioned networks are preferred for internal settlement due to their privacy features. However, if you need to interact with decentralized finance (DeFi) or offer public-facing wallets, a public Layer 1 is often necessary. Some hybrid approaches use a permissioned sidechain for private transactions and bridge to a public chain for final settlement.

As an Amazon Associate, we may earn from qualifying purchases.

Map the compliance framework

Building a private stablecoin requires more than technical infrastructure; it demands a legally defensible operating model. The regulatory landscape, particularly in the United States, is defined by overlapping authorities and active enforcement rather than clear, uniform statutes. To avoid regulatory friction, treat compliance as a foundational layer, not an afterthought.

The following steps outline the critical legal and operational sequences required to launch a compliant private stablecoin.

Start by selecting a jurisdiction with explicit stablecoin legislation or a clear regulatory pathway. The U.S. regulatory environment remains fragmented, with the SEC and CFTC often issuing guidance through enforcement actions rather than static rules. Countries like Singapore, Switzerland, and the EU (under MiCA) offer more predictable licensing frameworks. Choose a base that aligns with your target user geography and reserve currency.

Integrate Know Your Customer (KYC) and Anti-Money Laundering (AML) checks at the point of issuance and redemption. Unlike decentralized protocols, private stablecoins issued by fintechs like Circle or Tether Limited are centralized entities that must verify user identities. Use licensed third-party vendors to screen for sanctions lists and monitor transaction patterns for suspicious activity. This step is non-negotiable for maintaining banking relationships.

Establish a rigorous reserve management system. Reserves must be held in segregated accounts at regulated financial institutions. Engage a Big Four accounting firm or a specialized crypto auditor to provide monthly or quarterly attestation reports. Transparency here is your primary defense against claims of insolvency. Ensure your custody solution meets institutional-grade security standards, including multi-signature wallets and cold storage protocols.

Apply for necessary licenses, such as Money Transmitter Licenses (MTLs) in the U.S. or an Electronic Money Institution (EMI) license in Europe. Prepare comprehensive disclosure documents that outline the token’s mechanics, reserve composition, and redemption rights. The SEC’s framework emphasizes that stablecoins function as securities or money market instruments in many contexts; ensure your legal opinion aligns with the specific classification of your token.

Integrate payment rails

Setting up private stablecoin infrastructure requires connecting three distinct layers: the token issuance, the wallet ecosystem, and the fiat bridge. The blockchain is the pavement, your smart contracts are the toll booths, and the fiat on/off ramps are the on-ramps that let traditional money enter the system.

Most businesses do not build this stack from scratch. Instead, they integrate existing infrastructure providers that handle the heavy lifting of compliance and liquidity. Stripe, for example, offers a unified API that handles stablecoin payments, allowing businesses to accept tokens while settling in fiat currency. This reduces the operational burden of managing volatile crypto balances directly.

Before touching user funds, your stablecoin contracts must be deployed on the target blockchain. For private or permissioned stablecoins, this often involves a consortium chain or a private layer on a public network. You must conduct a rigorous third-party security audit. In high-stakes financial environments, a single vulnerability can lead to irreversible loss. Treat the audit phase as a legal compliance checkpoint, not just a technical test.

Your users need a way to hold and move these tokens. Instead of building custodial wallets from scratch, integrate with established wallet-as-a-service providers. These providers handle key management, security, and user onboarding. Ensure your integration supports the specific standards of your stablecoin (e.g., ERC-20 for Ethereum-based tokens). This step creates the "toll booths" where transactions are initiated and verified.

This is the critical bridge between traditional finance and your stablecoin ecosystem. You need a provider that can convert fiat currency to stablecoins and vice versa. Look for providers with strong regulatory licenses and access to deep liquidity pools. Stripe and other major fintechs offer these rails, allowing you to accept stablecoin payments while settling in your local currency, effectively neutralizing exchange rate risk for your business.

Run comprehensive test cases that simulate real-world user behavior. Verify that deposits, transfers, and withdrawals process correctly across all layers. Test edge cases, such as failed transactions or network congestion. This phase ensures that your infrastructure can handle the volume and complexity of live payments without disrupting your core business operations.

Once these rails are integrated, your stablecoin infrastructure is ready for limited pilot testing. The next phase involves monitoring transaction metrics and refining the user experience based on real data. Regulatory compliance is an ongoing process, not a one-time setup.

Conduct market research

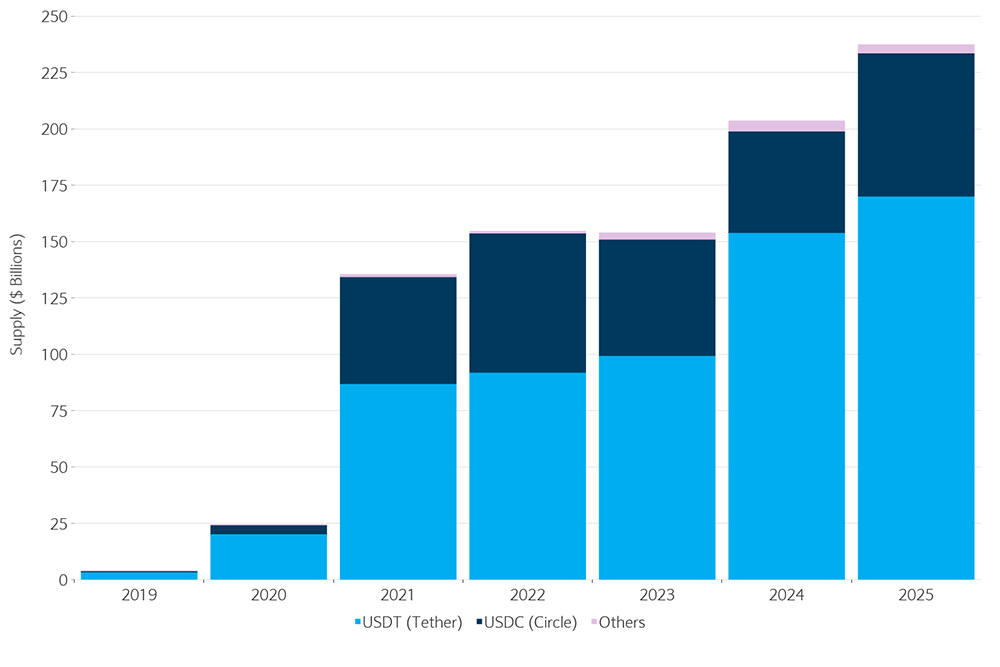

Before launching, understand who already holds the market. The private stablecoin space is dominated by a few major players, primarily Circle (USDC) and Tether (USDT). These are private companies that issue tokens in exchange for fiat deposits, manage reserves, and promise 1:1 redemption. Understanding their operational models is essential for benchmarking your own infrastructure and compliance requirements.

Market adoption trends show that stablecoins have evolved beyond simple fee-cutting tools. As noted in industry analyses, they are becoming a foundational layer for new financial software, enabling faster cross-border settlements and programmable money use cases. Your research should focus on how these larger players handle liquidity and reserve transparency, as these factors drive user trust.

To gauge current market sentiment and liquidity, monitor live price data for major private stablecoins. This helps you assess market stability and identify potential arbitrage opportunities or risks associated with de-pegging events.

Common questions about private stablecoins

Private stablecoins exist and handle the majority of on-chain volume, but they operate under a complex regulatory patchwork rather than a single federal law. Understanding how these tokens are issued and supervised helps you assess the risks of holding or using them.

These questions highlight the core tension in the sector: private issuers offer speed and global reach, but they lack the government backing that protects traditional bank accounts. Always verify an issuer’s reserve transparency before integrating their token into your infrastructure.

No comments yet. Be the first to share your thoughts!