Choose the right stablecoin model

Selecting the correct reserve structure is the first step in building compliant settlement rails. The model you choose dictates your regulatory exposure, liquidity depth, and counterparty risk. For enterprise settlement, the goal is predictable redemption and clear legal title over the underlying assets.

There are three primary private stablecoin models. Fiat-backed coins are backed 1:1 by cash and short-term government bonds held in regulated custodial accounts. Crypto-backed coins use overcollateralized digital assets to absorb volatility. Algorithmic coins rely on code and market incentives to maintain the peg, often without significant reserve backing.

| Model | Reserve Composition | Regulatory Risk | Liquidity Depth |

|---|---|---|---|

| Fiat-Backed | Cash, T-bills, commercial paper | High (banking-like oversight) | High |

| Crypto-Backed | Overcollateralized ETH, BTC | Medium (DeFi compliance unclear) | Medium |

| Algorithmic | No significant reserves | Low (but high failure risk) | Low |

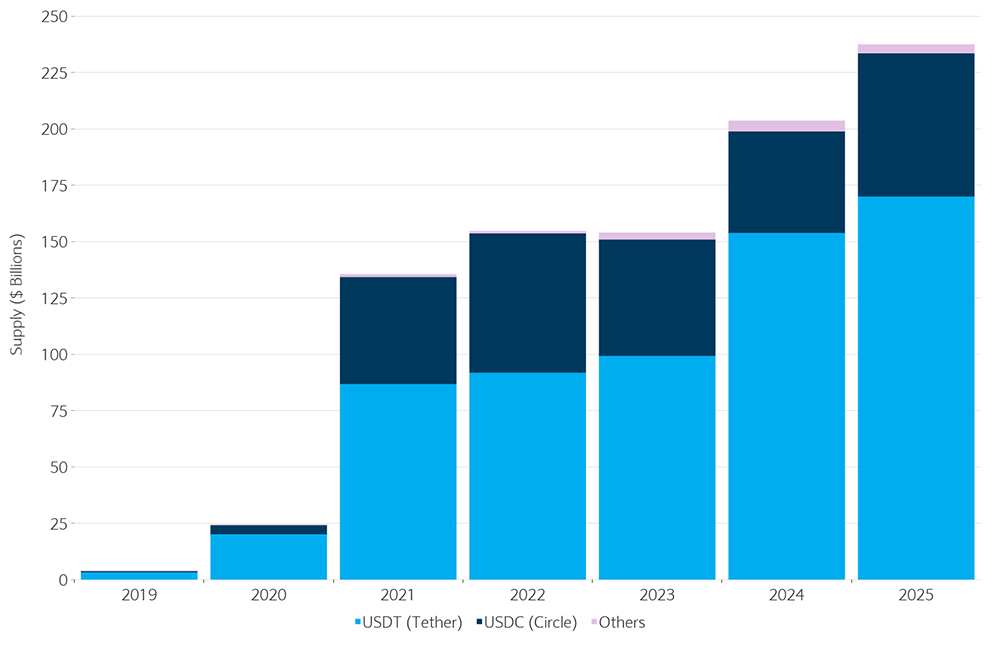

Fiat-backed stablecoins, such as USDC issued by Circle or USDT by Tether Limited, are the standard for private issuance. They offer the highest liquidity and the most straightforward path to regulatory compliance because they mirror traditional banking reserves. However, they require strict adherence to anti-money laundering (AML) and know-your-customer (KYC) regulations.

Crypto-backed and algorithmic models are generally unsuitable for enterprise settlement rails. Crypto-backed tokens introduce volatility risk that complicates accounting, while algorithmic models lack the reserve backing necessary for reliable redemption. For settlement, you need the stability and legal clarity that fiat-backed models provide.

Map the regulatory compliance path

Building compliant settlement rails requires a disciplined approach to legal classification and licensing. You cannot launch a stablecoin without first determining its legal status under both federal and state laws. The following steps outline the standard workflow for navigating the US regulatory landscape, with a focus on the SEC and state money transmitter requirements.

Start by analyzing whether your stablecoin qualifies as a security. The SEC’s framework evaluates whether users expect profits from the efforts of others. If your token is tied to a reserve managed by a central entity, it may fall under securities laws. Consult the SEC’s official guidance on digital asset classifications to assess your specific structure before proceeding.

Stablecoins are subject to state-level money transmitter laws in nearly every US jurisdiction. You must identify which states your users will access from and determine if those states require a Money Transmitter License (MTL). Some states have specific stablecoin legislation, while others rely on general fintech regulations. Map your target markets to understand the full scope of compliance obligations.

Regulatory frameworks for digital assets are evolving rapidly. Engage legal counsel with specific experience in blockchain and fintech compliance early in the development process. They can help interpret ambiguous regulations, draft necessary disclosures, and ensure your reserve management practices meet legal standards. Do not rely on general legal advice; specialized expertise is critical for high-stakes financial products.

Once your legal structure is defined, begin the application process for required licenses. This includes submitting MTL applications to state regulators and potentially registering with the Financial Crimes Enforcement Network (FinCEN) as a money services business. Prepare comprehensive documentation of your reserve assets, audit procedures, and anti-money laundering (AML) policies. The process is lengthy and requires meticulous attention to detail.

Navigating this path is not a one-time event. Regulatory expectations shift as agencies like the SEC and CFTC issue new guidance. Maintain an ongoing compliance review process to ensure your settlement rails remain compliant as the legal landscape evolves. Regular audits and transparent reporting are essential for building trust with regulators and users alike.

Select the settlement infrastructure

Choosing where your private stablecoin settles determines how fast money moves, how much it costs, and whether regulators can trace it. You have three main paths: public blockchains, permissioned ledgers, and hybrid setups. Each carries distinct trade-offs in transparency, speed, and compliance.

Public chains

Public networks like Ethereum or Solana offer deep liquidity and open access. However, they expose transaction data to everyone. For private stablecoins, this transparency conflicts with commercial confidentiality. You can layer privacy tools, but they often complicate regulatory audits. Public chains also face variable gas fees and finality times that can delay settlement during peak hours.

Permissioned ledgers

Permissioned ledgers restrict access to known participants. This structure aligns well with institutional requirements for privacy and control. Settlement is typically faster and cheaper than on public chains. The downside is limited liquidity and the need to build or join a consortium. You must manage identity verification and access controls internally or through a trusted provider.

Hybrid solutions

Hybrid models combine public and permissioned layers. Transactions might settle on a private ledger for speed and privacy, then anchor to a public chain for finality and auditability. This approach offers flexibility but increases architectural complexity. You need robust bridges and clear governance rules to prevent disputes between layers. Many large financial institutions are exploring this model to balance innovation with compliance.

Infrastructure selection checklist

Before committing to a settlement layer, verify these four areas:

- Scalability: Can the network handle your projected transaction volume without degradation?

- Finality time: Does the settlement speed meet your operational requirements (e.g., real-time vs. T+1)?

- Privacy features: Does the ledger support confidential transactions or zero-knowledge proofs if needed?

- Compliance tooling: Are there built-in or easily integrable KYC/AML checks and audit trails?

Stripe’s guide to stablecoin infrastructure notes that businesses must evaluate these factors against their specific risk appetite and regulatory obligations. FS Vector’s practical guide emphasizes that compliance tooling is often the deciding factor for institutional adoption.

Integrate payment rails and APIs

Connecting stablecoins to your existing financial stack requires bridging two distinct systems: the legacy banking world and the blockchain network. You aren't just sending tokens; you are building a compliant settlement rail that converts fiat deposits into on-chain value and back again. This process relies on specialized API providers and secure custody solutions to handle the heavy lifting of compliance and key management.

Don't build your own bridge. Use established payment processors like Stripe, BVNK, or FS Vector that already have the necessary banking licenses and compliance infrastructure. These providers handle the fiat on-ramps and off-ramps, ensuring that your transaction flows meet regulatory standards without requiring you to become a money transmitter yourself. Look for providers that offer real-time transaction monitoring and automated KYC/AML checks.

You need a place to hold the private keys that control your stablecoin assets. For integration testing and initial deployments, consider hardware wallets or enterprise-grade custody devices that support multi-signature requirements. This ensures that no single point of failure can compromise your funds. As you scale, you may need to integrate with institutional custodians who offer insurance and regulatory reporting, but for now, focus on securing the keys that interact with your payment APIs.

Use sandbox environments provided by your API partner to simulate transactions before going live. Test the full lifecycle: funding the wallet, sending a stablecoin payment, and confirming receipt on the blockchain. Verify that your internal ledger updates correctly and that webhook notifications trigger as expected. This step is critical for identifying latency issues or compliance flags before they impact real customers.

As an Amazon Associate, we may earn from qualifying purchases.

By following these steps, you establish a robust foundation for stablecoin payments. The key is to rely on existing infrastructure rather than reinventing the wheel, allowing you to focus on your core business logic while the API provider handles the regulatory complexity.

Monitor peg stability and liquidity risks

Your stablecoin’s value depends on trust, not just code. If the peg slips or liquidity dries up, settlement rails fail. You need a real-time dashboard to track both the price stability and the depth of the market.

Start by watching the live price feed. Even a 0.1% deviation from the $1.00 peg signals reserve stress or a liquidity crunch. Use a live price widget to monitor major private stablecoins like USDC and USDT against your local fiat pair. If your private stablecoin is new, compare its spread against these benchmarks to gauge market confidence.

Next, assess liquidity depth. A stablecoin can hold its peg in theory but fail in practice if there are no buyers when you need to sell. Monitor the order book depth on exchanges where your token trades. Thin order books mean high slippage, which erodes the value of your settlement transactions.

Keep an eye on reserve transparency reports. Private issuers like Circle and Tether publish regular attestations. Verify that your reserve assets match the circulating supply. If the issuer delays these reports, treat it as a red flag for potential de-pegging events.

Private stablecoin: what to check next

Private stablecoins are tokens issued by fintech companies rather than central banks. The most common examples are USD Coin (USDC), issued by Circle, and Tether (USDT), issued by Tether Limited. These private entities create tokens in exchange for fiat deposits, manage the underlying reserves, and promise 1:1 redemption to holders.

Building compliant settlement rails requires understanding that these issuers operate under private law frameworks. They are not government-backed, which means legal recourse for holders relies on the specific contractual terms and reserve transparency policies each company publishes.

No comments yet. Be the first to share your thoughts!